What affects your mortgage rate?

Your mortgage rate depends on many factors, like your property location, the economy, and loan size. One really influential factor is the amount you pay for your home loan. And fortunately, it's a variable over which you have complete control.

Homes for Sale in Kissimmee FL

When you pay more to have a lower rate, this is called "buying down" your mortgage rate, and the fees you pay are called "points." each point is one percent of the loan amount.

How do points drive your mortgage rate?

The relationship between your mortgage rate and its costs is an inverse one. When other factors are equal, a loan with higher fees has the lower interest rate. Home loans with lower rates are obviously more desirable, so it makes sense that they would cost more.

4 ways to keep mortgage closing costs low

Suppose you contact several mortgage lenders and are given these quotes for a $300,000 30-year fixed-rate home loan:

- 3.825 percent (no fees)

- 3.625 percent (.5 points)

- 3.500 percent (1.0 points)

- 3.375 percent (3.0 points)

You can see that the lower the rate, the higher the costs. But how do you know if the lower rate is a dream deal or expensive error?

The loan’s annual percentage rate, or APR, is helpful when you shop for home loans. It “equalizes” loans with various pricing and rates, using mathematical formulas. A loan’s APR includes not just its interest rate but also its costs.

Points and your annual percentage rate (APR)

The APR calculation allows you to compare loans with different rates and fees to see which plan costs you less. When a mortgage lender quotes you an interest rate or puts a rate in its advertising, it has to include an APR. (Hint: If the APR is significantly higher than the stated or advertised rate, it usually includes a lot of costs.)

Mortgage points: Are they worth it?

You'll probably notice that for the loan above, each extra point does not deliver the same reduction in rate. So some price points get you a better deal than others, and APR helps you find that sweet spot.

- 3.825 percent

- 3.665 percent

- 3.580 percent

- 3.613 percent

As your mortgage rate gets lower, it costs more and more to achieve further reductions. That's why the lowest rate here does not have the lowest APR.

Are points pointless?

It only makes sense to pay points when the benefit that you receive (the lower mortgage rate and payment over time) exceeds the added upfront cost.

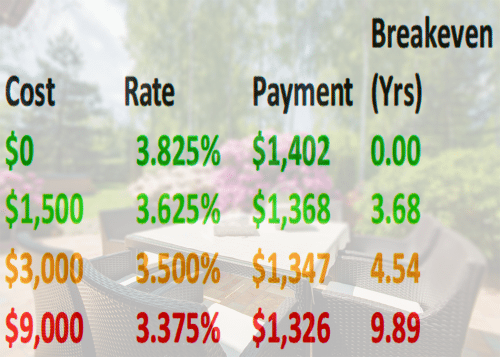

Here are the payments for each price point, and how long it takes for the monthly savings to make up for the added costs. For this example, the loan amount is $300,000.

You’ll also consider how long it will take for your monthly savings to pay for the cost of buying down your mortgage rate. In this case, the loan costing three percent, or $9,000, comes with a payment that is about $76 less than the payment of the zero-cost loan.

Misleading mortgage surveys: Why 3.79 percent costs more than 3.78 percent

By simply dividing the $9,000 cost by the $76 savings, you get 118 months. That means that it will take you nearly ten years before your savings outstrips the extra loan costs.

How your timeframe affects your APR

Whenever you pay upfront costs to get a mortgage, the APR calculation assumes that you spread those costs out over the entire life of the home loan. However, if you don’t keep the loan for its entire term, the APR disclosed as required by law is inaccurate.

That’s because you pay points upfront, but you won't realize all possible savings from the lower rate unless you keep the loan for its entire term.

How long will you keep the house?

That’s a good question, and one you should answer as best you can before choosing a mortgage.

How often, on average, do homeowners keep their houses? Longer than they used to, probably because the foreclosure crisis made it hard for people to sell and move.

Homebuyer tenure: How long are people staying in their houses?

In any event, the median number of years in a home in the US has increased from about six years in 2008 to about ten today, according to the National Association of Realtors.

If you’re completely in doubt, you’ll probably want to choose the mortgage with the fewest upfront costs.

What are today's mortgage rates?

Today could be a very good time to buy or refinance if your mortgage rate is right. Try comparing offers from several lenders now and see what kind of offer you can negotiate.

Show Me Today's Rates (Sep 1st, 2017)

Courtesy of Gina Pogol

The Mortgage Reports

Leave A Comment